PNC Bank Certificate of Deposit Rates: Unlocking the Secrets of High-Yield Savings

PNC Bank Certificate of Deposit Rates: Unlocking the Secrets of High-Yield Savings

PNC Bank, one of the largest financial institutions in the United States, offers a range of certificate of deposit (CD) options that cater to various savings goals and risk tolerance levels. With PNC Bank CD rates consistently ranking among the highest in the market, investors and savers are increasingly turning to the bank's CDs as a secure and profitable way to grow their wealth. In this article, we will delve into the world of PNC Bank CD rates, exploring the benefits, features, and options available to investors.

When it comes to growing one's savings, PNC Bank CD rates stand out from the competition. By locking in a fixed interest rate for a specified term, investors can earn a higher return on their deposits compared to traditional savings accounts. With terms ranging from a few months to several years, PNC Bank CDs offer flexibility and security that is hard to find elsewhere.

Understanding PNC Bank CD Rates

To make informed decisions about investing in PNC Bank CDs, it's essential to grasp the basics of CD rates and how they work. CD rates are determined by the market, and PNC Bank's rates are influenced by a combination of factors, including:

• **Market conditions**: The overall economic environment, including interest rates and inflation, affects CD rates.

• **Term length**: Longer-term CDs typically offer higher rates, as the bank is locking in a deposit for a longer period.

• **Balance requirements**: Some CDs require a minimum deposit to open, and the balance may impact the interest rate offered.

• **Early withdrawal penalties**: CD rates may be higher if the account holder is penalized for early withdrawal.

By understanding these factors, investors can make informed decisions about which PNC Bank CD is best suited for their needs.

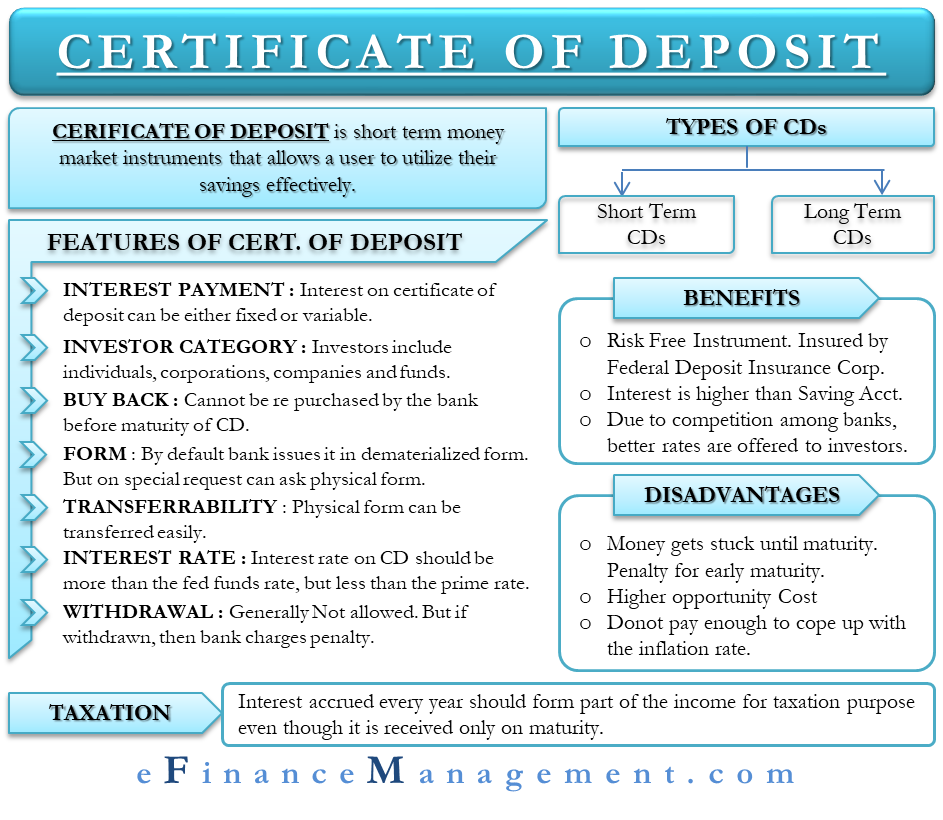

Types of PNC Bank CDs

PNC Bank offers a variety of CDs that cater to different investor profiles. Some of the most popular options include:

• **Traditional CDs**: These are the most basic type of CD, offering a fixed interest rate for a specified term.

• **No-Penalty CDs**: These CDs allow investors to withdraw their funds before the term ends without incurring an early withdrawal penalty.

• **Jumbo CDs**: Higher balance requirements are often associated with higher interest rates on these CDs.

• **Step-Up CDs**: These CDs allow investors to take advantage of higher interest rates if market conditions improve during the term.

• **IRA CDs**: PNC Bank offers CDs specifically designed for individual retirement accounts (IRAs), providing a tax-advantaged way to save for retirement.

PNC Bank CD Rate Comparison

When comparing PNC Bank CD rates to those of other financial institutions, it's essential to consider the terms and conditions associated with each account. Here's a snapshot of PNC Bank's current CD rates compared to some of its competitors:

| Term | PNC Bank Rate | Competitor Rate |

| --- | --- | --- |

| 6-month | 2.50% APY | 2.20% APY |

| 1-year | 3.00% APY | 2.80% APY |

| 2-year | 3.50% APY | 3.10% APY |

| 3-year | 4.00% APY | 3.40% APY |

As this comparison illustrates, PNC Bank CD rates are consistently higher than those of its competitors, making it an attractive option for investors seeking high-yield savings.

Tax Implications of PNC Bank CDs

CDs are a low-risk investment, but it's essential to consider the tax implications of investing in a PNC Bank CD. Interest earned on CDs is subject to federal income tax and may be subject to state and local taxes. However, some CDs, such as those in IRA accounts, provide tax benefits that can help reduce the tax burden.

"To minimize taxes on CD interest, it's essential to understand the tax implications and optimize your CD investment strategy," advises Chris Herman, a certified financial planner with PNC Wealth Management. "By considering factors such as tax brackets and withholding, investors can make informed decisions about their CD investments."

PNC Bank CD Minimum Balance Requirements

To open a PNC Bank CD, investors typically need to meet minimum balance requirements, which can vary depending on the type of CD and term length. Here are some common minimum balance requirements for PNC Bank CDs:

• **Traditional CDs**: $1,000 to $10,000

• **No-Penalty CDs**: $1,000 to $5,000

• **Jumbo CDs**: $100,000 to $250,000

• **IRA CDs**: $1,000 to $5,000

PNC Bank CD Fees and Penalties

PNC Bank CDs are designed to be low-risk investments, but investors should be aware of the fees and penalties associated with early withdrawal. Some common fees and penalties include:

• **Early withdrawal penalty**: 1% to 3% of the principal amount

• **Maintenance fees**: $10 to $25 per month

• **Overdraft fees**: $30 to $35 per overdraft

Investors should carefully review the terms and conditions associated with their PNC Bank CD to understand any fees or penalties that may apply.

Conclusion

PNC Bank CD rates are an attractive option for investors seeking high-yield savings with low risk. By understanding the basics of CD rates, the types of CDs available, and the tax implications, investors can make informed decisions about their CD investments. While PNC Bank's rates may not always be the highest, the bank's competitive rates, flexible terms, and comprehensive suite of CDs make it a solid choice for savers and investors. As Tom Folliard, senior vice president of retail banking at PNC Bank, notes, "Our CD rates are designed to provide investors with a secure and profitable way to grow their wealth. With our competitive rates and flexible terms, PNC Bank CDs are an attractive option for anyone seeking high-yield savings."

Related Post

Dirty Grandpa: The Unlikely Stardom of Robert De Niro's Latest Role

Demystifying the Texas Police Scanner: A Key to Unlocking Public Safety and Transparency

The Troubled Story Of Ron White's Battle With Alcoholism: A Comedian's Descent Into Darkness